Something very unusual took place in 2014, that changed the course of the global economy. In June 2014, global oil prices began to fall. Brent Oil prices almost reached $115 in late June, and then began to fall precipitously. In early October 2014, with Brent prices about 20% lower at $90 per barrel, the PIRA Energy Group held a seminar in New York City that was attended by a Saudi delegation led by Nasser al-Dossary. At that time, when asked if the Saudis were going to cut supplies to protect prices, Dossary was reported to have commented ,

“What makes you think we’re going to cut?”.

That statement incited international headlines. Saudi did not cut its production and oil prices continued to crash – falling two thirds to under $30 per barrel in January 2016 before rising again.

Why did Saudi change its policy, established over decades, to stem the fall in crude prices?

There are several potential reasons for this. Let us examine each in detail.

Moving away from Fossil Fuels

As the world wakes up to the dangers of climate change, a common point of agreement is that we need to reduce our use of fossil fuels.

On the face of this, this looks like an impossible ask. The world gets 80% of its energy from fossil fuels, the cost of energy produced from fossil fuels is cheaper than from alternate sources and the infrastructure: to produce and use fossil fuels is very long lived: some of it lasting beyond 50 years.

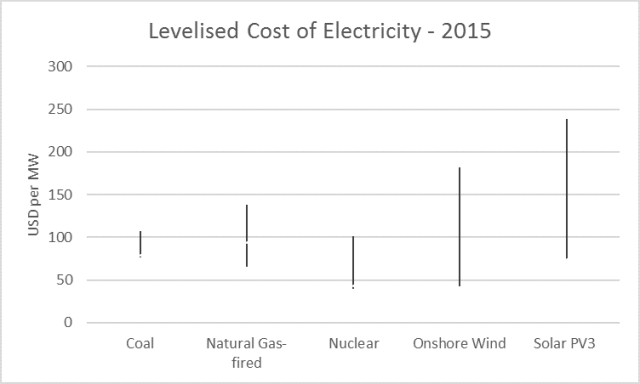

While we will explore the concept of levelised costs of different sources of electricity in the chapter on Solar Power, Figure 1 presents the comparison now .

Figure 1: Levelised Cost of Electricity from OECD countries and China, 2015

Figure 2: Share of Total Primary Energy Supply by source

However, if we want to restrict our planet’s warming within the 2C limit, much of the fossil fuels available under the ground today will have to stay under the ground. Because 80% of greenhouse gas emissions come from burning fossil fuels . Just how much will have to be stranded?

An authoritative study published in the highly respected Nature Journal said that globally, a third of oil reserves, half of gas reserves and over 80 per cent of current coal reserves should remain unused from 2010 to 2050 in order to stay within a 2°C warming limit .

This struck the first blow against fossil fuel producers.

But this might have remained just impotent cries from scientists had it not been for one more thing: the updated burning embers chart in the IPCC report showed all countries would suffer if we exceeded the 2C limit.

So, the road to Paris was substantially different from the past.

Countries joined the bandwagon on the way to the Paris Climate Summit, with many pledging lowering of either their overall emissions and/or specifically lowering the fossil fuel intensity of their energy use.

India has put forward the targets to lower the emissions intensity of its GDP by a third by 2030 (below 2005 levels) and to increase the share of non-fossil based power generation capacity to 40% of installed electric power capacity by 2030. While the latter is negative for coal, the former is negative for oil as well, given India’s stated aim of enabling public transport with a lower crude oil footprint. Separately, India has taken concrete reforms to reduce her dependence on fossil fuels: by increasing excise duty on petrol and diesel, quadrupling the coal cess from Rs.50 per tonne to Rs.200 per tonne and Prime Minister Modi’s plan to increase the production of solar energy to 100 GW by 2022 .

The USA has committed to a reduction of 26-28% greenhouse gas emissions by 2025. Given that its transportation sector accounts for over quarter of its emissions and relies on almost entirely on oil, this is crude-negative.

“No challenge – no challenge – poses a greater threat to future generations than climate change…We believed we could reduce our dependence on foreign oil and protect our planet… Every three weeks, we bring online as much solar power as we did in all of 2008. And thanks to lower gas prices and higher fuel standards, the typical family this year should save $750 at the pump.” Said Obama in his sixth State of the Union address in January 2015.

China, for its part, committed to lower the carbon intensity of GDP by 60% to 65% below 2005 levels by 2030, increase the share of non-fossil energy carriers of the total primary energy supply to around 20% by that time .

Countries were beginning to reduce their use of fossil fuels – they were expressing themselves through announcements and regulatory action.

Shift in Investment

Governments were joined by other influential decision makers. What began in 2011 with college students protesting to demand their institutions to shift away from fossil fuel investments has now grown to include sovereign wealth funds, pension funds, family offices and religious institutions. All told, by September 2015, over 400 institutions representing $2.6 trillion in assets, pledged to reduce or exit from their fossil fuel institutions .

Ironically, the Rockefeller family fund, whose family fortunes derived from oil, declared its intention to exit any fossil fuel-based asset “as quickly as possible”. The announcement that accompanied this decision was quite blunt:

“While the global community works to eliminate the use of fossil fuels, it makes little sense—financially or ethically—to continue holding investments in these companies.”

“We would be remiss if we failed to focus on what we believe to be the morally reprehensible conduct on the part of ExxonMobil. Evidence appears to suggest that the company worked since the 1980s to confuse the public about climate change’s march, while simultaneously spending millions to fortify its own infrastructure against climate change’s destructive consequences”

Populist movements and shift in Investment

In June 2015, Norway’s parliament formally endorsed its $900 billion fund to sell off its coal assets . In October 2015, the Financial Times reported Yngve Slyngstad, chief executive of the oil fund, saying “If you run a sovereign wealth fund in a democracy and there are limits to what the population wants to make money on. That they [politicians] first removed tobacco and certain types of weapons and now have removed coal is of course a reflection of the Norwegian population’s sentiments and instincts with regard to where we want to make money for our grandchildren.”

In April 2016, Norway’s oil fund excluded 52 companies for being too reliant on coal. The war on fossil fuel divestment had been well and truly joined.

The Church entered the fray with Pope Francis’ encyclical.

“We know that technology based on the use of highly polluting fossil fuels – especially coal, but also oil and, to a lesser degree, gas – needs to be progressively replaced without delay ”

This played no small part in the Church of England pulling out of coal and tar sands investments in its £9 Billion fund .

The popular sentiment was against fossil fuel use. And they were expressing this financially.

Shifts in Demand

Energy defines our lives today. As people and countries become wealthier, energy use first increases rapidly and then plateaus off or falls. Consider this: a poor farmer sends his daughter to college and then she gets a job in a multinational bank. Initially everyone in the farmer’s family would have either walked or taken a bus. They would have cooked in a wood-fired stove, and bought few clothes for Diwali. His daughter probably stays in a working-woman’s hostel and commutes to work in a spanking new two-wheeler. The family walks less and uses the bus more. They perhaps visit her in the city – travelling by train for the occasion and enjoy shopping and visiting malls.

But in the US or Germany, people maybe buying better insulation for their houses, going for more energy efficient appliances, so their energy consumption falls even while their “well-being” increases. You don’t add a second air conditioner in a room or drive in two cars. You might even adopt a solar powered Tesla as the new symbol of cool.

But the world has been consuming fossil fuels voraciously.

World demand for Crude Oil has grown from 80 million barrels per day (bpd) in 2003 to 94 million bpd in 2015 . Global coal consumption increased by more than 70% from 4600 Mt in 2000 to an estimated 7 876 Mt in 2013, and at a 4.2% annual rate – driven almost entirely by China .

But as in all things, totals and averages hide a fascinating diversity of detail.

First demand is falling in developed (OECD) countries who account for half of crude demand. Crude demand has fallen 10% in these countries in this period to just over 46 million bpd. Coal consumption in OECD countries has fallen by nearly 10% from 2002-2012 .

This is being driven in part by energy efficiency improvements, a shift to using natural gas and in part by warmer winters which is reducing the need for heating.

“If you look at the 24-year period, there is some warming in Europe and this has contributed to lower heat demand and lower greenhouse gas emissions,” said Ricardo Fernandez from the European Environment Agency. “In the last two years it has even been stronger in 2014 you can see that, while it’s not the only factor, by and large it’s due to the milder winter conditions in Europe.”

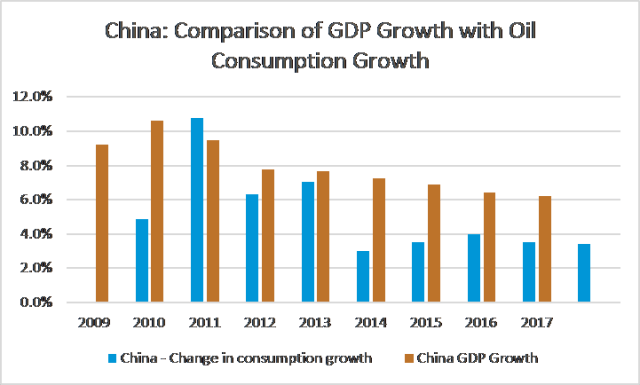

So the demand increase in the past decade was lead almost entirely by the growth of China and India. Chinese demand doubled in this time frame from 5.6 bpd to over 11.3 million bpd in 2015, while Indian demand growth has been slower in this period, growing from 2.5 million bpd in 2003 to 3.7 million bpd in 2014.

China’s demand for coal and crude is beginning to slow – faster than the economy is slowing, driven by shifts to less energy-intensive industries, to more renewable power, gains in efficiency and improving technology.

Indeed, Chinese energy-related greenhouse gas emissions declined by 1.5% in 2015, as coal use dropped for the second year in a row. In 2015, coal generated less than 70% of Chinese electricity, 10% less than in 2011. Over the same period low-carbon sources jumped from 19% to 28%, with hydro and wind accounting for most of the increase .

The other issue is efficiency; older coal plants operate at an efficiency of around 30% while newer plants operate at efficiencies closer to 45%. This means upgrading older plants will result both in savings of coal and CO2 emissions . China has been upgrading its coal plants aggressively.

Figure 3: Chinese Oil Demand decoupling from GDP Growth

India is a big user of fossil fuels with a demand set to grow. India’s power is largely coal dominated, while her transportation network is driven primarily by oil and coal.

An estimated 240 million Indians do not have access to electricity today and several hundred million Indian households use wood-fired cook stoves that are very dangerous to health as their primary cooking medium . Also as Indians become wealthier and move to cities, their use of energy will grow: appliances, transportation and spending all improve as India becomes more urban and more wealthy.

The advantage India possesses is that it is beginning its development journey well after other countries, so it gets to “leapfrog” technologies – this is when countries can gain development while using newer and better technologies than the ones used by countries starting first.

An example might help: while India’s power is still largely produced by burning coal, India has access to newer technologies like gas-fired plants, windmills, or utility-scaled solar or even much more efficient coal plants. This way it can generate power in a less warming and less polluting fashion than say, England in the early 1800s. India’s coal is of very poor quality with high ash content that leads to very low efficiency. This makes a transition to either solar or more easily, natural gas more attractive on an economic basis.

India is building 20 km of roads every day in 2016. This could soon go up to 30 km of road per day as per Nitin Gadkari, India’s Road Transport and Highways Minister . In FY16, India added more than 20 million new vehicles on those roads.

But India’s energy intensity of GDP is declining. The energy intensity of the economy has decreased from 18.16 goe (grams of oil equivalent) per Rupee of GDP in 2005 to 15.02 goe per Rupee GDP in 2012, a decline of over 2.5% per annum despite a robust GDP growth in that period.

And India’s transportation sectors greenhouse gas emissions are a tiny fraction (0.3% in 2011) of overall global greenhouse gas emissions . Even if India were to double her transportation greenhouse gas emissions, this would not wreck the carbon budget.

There is another very real barrier to the increase of crude oil in countries like India. Congestion and convenience. A ride in one of Bangalore’s roads at almost any time of the day or in Delhi is enough to demonstrate this point in smoky, congested detail. In a study conducted by the Consortium of Traffic Engineers and Safety Trainers and reported by The Hindu shows that average vehicle speeds in Bangalore fell from 35 kmph in 2005 to 9.2 kmph in 2014. Data from IIT Madras, shows that vehicle speeds in Chennai (SP Road) fell from 49 kmph in 1992 to 20 kmph in 2014. This cannot continue. Something has to give – which is probably a shift to public transportation – either by bus (preferably) or to a metro. The latter can be powered off the grid, again lowering the need for crude while the former will place the crude demand on a much slower trajectory than the present.

India has also turned into a power-surplus country in 2017 after a gap of 8 years. Anyone who has spent the past few years in Tamil Nadu can attest to the fact that power cuts have reduced substantially. This, along with the introduction of the UDAY scheme of debt-restructuring for State Electricity Boards is set to sharply reduce the demand for diesel generator sets – another negative for crude demand.

Lastly, India has launched several energy efficiency schemes – notably the UJALA scheme whereby the government supplies LED bulbs at highly discounted rates to customer with a metered connection. To date (July 2016), more than 128 million lights have been distributed resulting in an energy saving of over 45 million units per day. Other schemes include changing agricultural pump sets to solar-powered pump sets and encouraging adoption of energy-efficient appliances.

This means India’s power demand will grow, no doubt. But it will grow slower than GDP growth and in a less carbon-intense way. The rise of solar will play a major role in India’s energy roadmap.

The rise in solar

The IEA preliminary data suggest that electricity generated by renewables played a critical role, having accounted for around 90% of new electricity generation in 2015; wind alone produced more than half of new electricity generation. In parallel, the global economy continued to grow by more than 3%, offering further evidence that the link between economic growth and emissions growth is weakening .

Solar power has had a dramatic transformation in the past decade. For India, capital costs of solar have plunged 70% from Rs. 18 million per MW to Rs. 5.3 million per MW in 2016 . Prices have fallen since. Replacement costs for coal are still much lower at Rs. 1.2 million – but these do not include the costs of pollution from coal.

Another way to consider this would be to look at levelised cost. This is the cost per unit of electricity generated from a given source taking into account capital costs, running costs, subsidies and pollution costs.

The buzz around Solar power in India hummed loudly on the announcement of reaching a 100 GW target by 2020. That was a INR 6 Billion announcement! That got all the foreign players interested. The rates fell rapidly in 2015 and into 2016.

In July 2015, Canadian Firm, SkyPower placed a “paradigm-shifting” bid of Rs. 5.05 per unit generated for a 50MW utility plant in Madhya Pradesh. Around that same time, many corporates were negotiating rooftop solar tariffs of between Rs. 6.50 to Rs. 7.20 per unit for 25 year agreements.

But this was not a unique event. In September 2015, Photon Solar won a 50 MW project in Punjab with a winning bid of Rs. 5.09.

Then came Sun Edison’s bid of Rs. 4.63 for a 500 MW project in Andhra Pradesh in November. The Livemint newspaper reported a comment from Pashupathy Gopalan, president, Sun Edison Asia Pacific “There are 15 or 20 companies that are in the same ballpark in their bids (as SunEdison). We are not particularly aggressive.”

Prices fell further. In 2016, for a 420 MW project in Rajasthan, several bidders quoted below Rs. 5/unit and the winning bid was Rs. 4.34 per unit.

Solar was now cheaper than coal.

Power Minister, Piyush Goyal tweeted “Through transparent auctions with a ready provision of land, transmission and the like, solar tariffs have come down below thermal power cost” .

In November of 2015, the consulting firm, KPMG released a report titled “Rising Sun” in which they stated that by 2025, solar would be substantially cheaper than coal! In hot countries like India with large T&D losses, solar is an easy choice to make – especially decentralized solar.

And the technology is improving every month. The next battle to be won is the battle in electricity storage. There are exciting advances being made here, which we shall consider later.

The death of king coal is not very far away.

The electric car

But Crude Oil is a different story. You see, crude oil goes into transportation, and until recently electric cars were a bit of a joke that even passionate environmentalists had a difficult time buying into.

Then came Tesla. With a turnover of over $4 Billion in 2015, and with a roadmap to profitability, Tesla made very cool, sexy and desirable cars. By the way, the cars ran on electricity.

Once in a while, you get one of those people who question the way things are done. Even more rarely, some of these questioners are imbued with a tremendous sense of energy, purpose and execution skills. They are the juggernauts that disrupt industries and the world.

One such person was Elon Musk. His entrepreneurial journey and love of space started early. At age 12, he programmed a space-themed PC game called Blastar which he sold for $500 to the magazine PC and Office Technology. Musk emigrated to Canada and then transferred to the University of Pennsylvania to complete double-bachelors in Physics and Economics. While in college, he and his best friend rented a frat house to run as an informal night club .

Shortly after dropping out of a PhD program in Stanford, Musk and his brother, Kimbal, started Zip2 developed and marketed an Internet “city guide” for the newspaper publishing industry. They had very little money at that time.

“Things were pretty tough in the early going” recalled Musk while speaking in 2003 at a Stanford University Technology Ventures Program. “I didn’t have any money…I couldn’t afford a place to stay and an office. So, I rented an office instead…and I just, sort of, slept on the futon and showered at the YMCA.”

Musk eventually sold Zip2 to Compaq for over $200 Million, pocketing $22 million in the process. His love for cars was evident in the fact that he used some of the money to buy a $1 million McLaren F1 car.

He also used the money to set up X.com, that later became Paypal. eBay acquired Paypal for $1.5 billion in stock in 2002 . Musk finally entered the big league.

Exiting Paypal left a void, and Elon Musk was still pursuing “Change the World” dreams. Influenced by Asimov, he wanted humans to populate other planets. This lead him to form Space-X. He was also very concerned about climate change and wanted to do something about it.

“I think global warming is a very serious issue and something that we have to address and the only way to address to address that is to come up with a car that doesn’t add Carbon emissions to the environment. And I think the way to do that is through electric vehicles.”

While electric vehicles do add carbon emissions to the environment depending on the fossil fuel content of the grid feeding them power, they had one big advantage. They displaced petroleum or diesel as a fuel source. This is a big deal – because grids could more easily be powered by low carbon sources than a car can.

Tesla was started in 2003, and not by Elon Musk. Indeed, Musk was an early investor who then transformed into the Chairman and later CEO. The first car in Tesla’s stable was the Roadster, a zippy, expensive sports car which appeared on the cover of Time Magazine in 2006 . In an August 2009 edition of The New Yorker, Lutz was quoted as saying, “All the geniuses here at General Motors kept saying lithium ion technology is 10 years away, and Toyota agreed with us—and boom, along comes Tesla. So I said, ‘How come some tiny little California startup, run by guys who know nothing about the car business, can do this, and we can’t?’ That was the crowbar that helped break up the log jam.”

Tesla then launched its multiple award winning model, the Model S in 2012. With over 100,000 vehicles sold to date, the Model S was one of the bestselling electric cars ever. Tesla followed this up with a Model X, an electric-powered SUV in 2015, with a mass market Model 3 opened for pre-booking in March 2016. Within a few days, more than 230,000 customers had pre-booked a vehicle, each pre-booking order needing a $1000 deposit !

Musk’s Alpha male persona was fully evident in the fact that the models names strung together read “S3X”.

A question I often get asked is “Are electric vehicles green?”. My answer is to say that it depends almost entirely on the grid feeding the electricity to the car. If the grid is powered largely by coal, then, no, an electric car is not green.

For India, based on the information from the Ministry of Power, our grid is about 60% coal-powered, 16% hydel, 12% “Other renewable” and 9% gas . In reality, the share of coal in generated units is probably a little higher, given that wind and hydel tend to be seasonal. The Central Electrical Administration has used emission factors to arrive at a 0.82 tons of CO2 per MWh of power generated . This means that for every unit of electricity generated, 820 grams of CO2 are emitted. Please note than other greenhouse gases are emitted but not captured in this estimation.

But the electric car is not charged at the point of generation. It is charged at our homes or offices. So the electricity has to travel all the way from the point of generation to the point of use, subjecting itself to a transmission and distribution loss. In India, this is about 23% officially and much higher unofficially. Some part of the loss is technical – i.e., losses that are physical in nature – due to friction, heat and other line losses caused both by the nature of transmission and by the aging equipment or overloading. The other part is “commercial” – units that are generated and used but not paid for – these include theft, agricultural units etc. There can be many points of view on how to assign the emissions caused by “lost” units, but, at the very least, we need to account for transmission losses when calculating the CO2 emissions emitted when a unit of electricity is consumed.

Using the above, the CO2 footprint (or the grams of CO2 emitted per kilometre travelled) is comparable for a Reva e20 at ~100 grams per km and a Nano at ~ 115 grams per km or a Maruti Alto 800 at 120 CO2 per km based on similar assumptions of driving conditions. This assumes that the Reva gives 90 km for a full charge, while the Nano does about 20 km per litre and the Alto, ~ 19 kmpl. Moreover, several studies show that if we were to add manufacturing CO2 emissions, or the emissions involved in making a car, an electric car in India has larger CO2 lifetime emissions than a comparable petrol car.

Most exciting is a recent announcement by Hanergy, a leading thin-film solar power company. They were using thin film solar panels – flexible solar panels, essentially to fashion a care that could charge itself. The company announcement said that 5-6 hours of sunlight was enough to allow the car to travel 80km on sunlight alone . The car is yet to be launched and the claims are yet to be tested. But if true, then zero-priced crude is not far away.

The journey will not be smooth

Coming back to why Saudi refused to cut. Consider the position of Saudi Arabia. As it stands, Saudi Arabia is facing “peak demand” – a prospect of continually falling crude oil demand even as the world economy grows – there’s a real chance that much of the oil under the ground may remain buried forever. With over 212 billion barrels of reserves, that’s a lot of oil to be left stranded.

And why should Saudi Arabia be the one to cut? Even at a $20 oil price, over 60% of Saudi’s reserves remain profitable to extract, while less than 1% of USA’s or Russia’s reserves are profitable to extract. While Saudi Arabia faces a budget shortfall at current oil prices, it has $700 billion reserves as a palliative to ease the pain. Moreover, its competition would feel more pain – Iran for instance. Just a third of Iran’s 128 billion barrels would be profitable to extract at $20 and Iran does not have the reserves that Saudi has.

Importantly, Saudi no longer has full control over the competitive dynamics of oil producers. They no longer form an effective cartel – they are too diverse. It’s highly unlikely that the entrepreneurial private American shale producers would follow Saudi’s lead in cutting. Nor would Russia or Iran.

Indeed, Iran’s re-entry into the global crude market in 2016 made for a structural shift in the market. For a decade, Iran had faced sanctions from the world for its pursuit of its nuclear weapons program. These sanctions were enhanced in 2012, when Iranian banks identified as institutions in breach of EU sanctions were disconnected from the SWIFT , the world’s hub of electronic financial transactions. In the same year, the EU said agreed to an oil embargo on Iran and to freeze the Iranian Central Bank’s assets. Sanctions tightened further when major super tanker companies said they would stop loading Iranian cargo. EU sanctions made European insurers, who dominated the marine insurance sector, from offering cover on Iranian crude. This insurance ban will affect 95 percent of the tanker fleet because their insurance falls under rules governed by European law. Historic negotiations ensued – which resulted in January 2016’s announcement by the International Atomic Energy Agency that Iran had adequately dismantled its nuclear program leading to lifting sanctions. Iran had re-entered the global crude markets.

Iran has large low-cost reserves – second only to Saudi Arabia. And it is not overly fond of the Saudis and unlikely to take their lead.

There was thus no competitive sense in cutting. This fact was echoed in the Saudi’s erstwhile Petroleum Minister’s statement. On 4th March 2015 in Berlin, Ali al-Naimi, a legendary figure in the world of oil, said

“Over the past eight months, though, with the market in surplus, it is Saudi Arabia that is called upon to make swift and dramatic cuts in production. This policy was tried in the 1980s and it was not a success. We will not make the same mistake again. ”

So what

Does this mean that crude and coal prices will assume a linear path to zero? Of course not. Oil reserves are concentrated in some of the most volatile places on the planet that are prone to daily violence. If the violence escalates, crude prices will shoot up. Many coal mines and oil rigs remain susceptible to climatic forces such as storms and flooding. These could also cause disruptions that would serve to price spikes.

As prices fall and some countries restrict their use of coal, the very cheapness of coal will ensure that it remains a preferred energy source for developing nations for a long time to come. Once a coal plant is built, it continues to produce as long as it covers marginal costs – or the costs incurred in producing just one additional tonne of coal from the plant . Consider what happened in 2016. European nations had cut their consumption of coal – both for environmental reasons and because natural gas was available at a cheaper price. China was reducing its coal production by restricting the number of days a plant could operate in a year – primarily because of the polluting effects of coal plants .

That caused a spike in international coal prices. But would that be long lived? Unlikely. India made an announcement in the middle of 2016 that it had sufficient coal to meet its domestic needs and was entering the international markets as an exporter. In an oversupplied market like coal, that’s what happens – when prices spike temporarily supply that has been paused re-enters the market to drive prices down again.

The true death knell for coal will come when energy storage options become much cheaper. This will make solar a competitive option for base load. What is base load? Electricity demand varies over the course of a day and over a year. For instance, energy use typically peaks in the day in India in summers as cooling needs are highest. While energy use peaks in winters in colder climates as heating needs increase. Base load is the minimum power required to be supplied throughout the day. Today base load is supplied by coal, natural gas, oil or nuclear. Renewable sources of energy are often seasonal or have a clear daily variation – the sun only shines in the day! But having a cost effective means of storing the energy would mean, renewables can start supplying base load and finally edge out fossil fuels.

What does this mean for India?

In many ways, the fall of crude and coal prices is a huge positive for India.

The first is a much lower import bill.

Consider this. Imports supply most of India’s crude oil consumption. While India’s consumption of crude oil-derived products like diesel or natural gas has been increasing, her domestic production of crude oil or gas has been steadily decreasing. Thus, India is increasingly becoming dependent on imports.

As such, a fall in international crude prices is one of the largest macro-economic positives for the Indian economy. Indeed, as per news reports, India’s crude oil import bill in FY16 nearly halved to $64 billion from $112.7 billion in FY15 even while the quantity imported increased nearly 7% to 202 MT . In Rupee terms, that’s a saving of more than Rs. 2.5 Lakh crores . While some of this saving was passed onto the Indian customer as lower prices, a large part was retained by the centre. This helped balance the budget to no small extent.

But there is another big saving for India and that has to do with subsidies. India’s major subsidies relate to food, petroleum and fertilisers. The combined subsidies on these three is greater than Rs. 3 lakh crores (or $95 Billion) in FY14 or about 5% of the GDP of that year.

Subsidies on petroleum products, which include subsides on diesel, kerosene and LPG, fell almost 80% from nearly Rs. 1.5 lakh crores in FY14, to just over Rs. 22,000 crores for 9 months in FY16 .

The fall in the subsidy burden has created a fiscal space that is a necessary (but not sufficient) first step in infrastructural improvements that India stands in crying need of.

There is another positive cycle that lower crude prices have set off. They have forced substitutes such as solar and coal to quote lower prices to retain their competitive positions. For instance, I doubt the solar bids would have been quite so aggressive had coal or crude prices been higher. This results in a lower net power costs for all manner of consumers – individuals and institutions.

Individuals travel more. Air travel has become cheaper and more popular as air turbine fuel prices have fallen. This in turn has strengthened the financial position of airlines and the loan positions of banks that lend to them. The poor, who face highly subsidised rates of petroleum products, have not gained because of crude or coal price fall, while most customers have not face the benefit, because retail prices have hardly fallen 15% or so from mid-2014 to now .

Unless lower energy prices are coupled with enforcing strict market discipline on our unwieldy state electricity boards, the consumers – individuals and companies – are unlikely to reap the full benefits of long term lower prices unless the buy directly from third party power producers or invest in roof top solar systems.

Energy Prices are falling in conjunction with another important trend: automation is rising. As automation grows in nature and in presence, even countries like India will opt to automate their processes. Take textiles, the second largest employer after agriculture in India. Modern textile mills have cut their employment progressively across the value chain – they do this in spite of low labour costs so as to ensure quality and to reduce dependence on a highly unpredictable labour force. Call center jobs are in jeopardy of losing out to “chatbots” – Artificial Intelligence software that can replace them. Lower energy prices tilt the choice towards investing in automation – not a good when India’s labour force is growing a third faster than the number of jobs available .

But before we celebrate, there is one big short term negative for India – one that is already being felt. Remittances are an important source of capital for India, and an important part of economies of states like Kerala that sends so many to the Gulf each year. India received $30 Billion in 2012 from the Middle East – almost half its total inward remittances for that year. That trend, thanks to the oil boom ending, is now reversing.

While writing this, I was asked, is this fall a good opportunity? Should India secure long term contracts at low prices now, before prices move up. My answer would be no. While $40 crude may look cheap to $140 crude, I will stick my neck out and say the world is a different place in 2016 than it was in 2011. Solar has turned the corner, Climate Change is increasingly being perceived as being an existential threat and fossil fuels are in an excess supply mode. Crude and Coal will fall. Let’s not try and catch a falling knife.